The Housing Market Is Locked

Why 3% mortgages are freezing supply and keeping prices stuck

A strange thing is happening in housing right now.

Rates have more than doubled.

Affordability has worsened.

And yet… prices haven’t fallen the way many expected.

Why?

Because the housing market didn’t break. It locked.

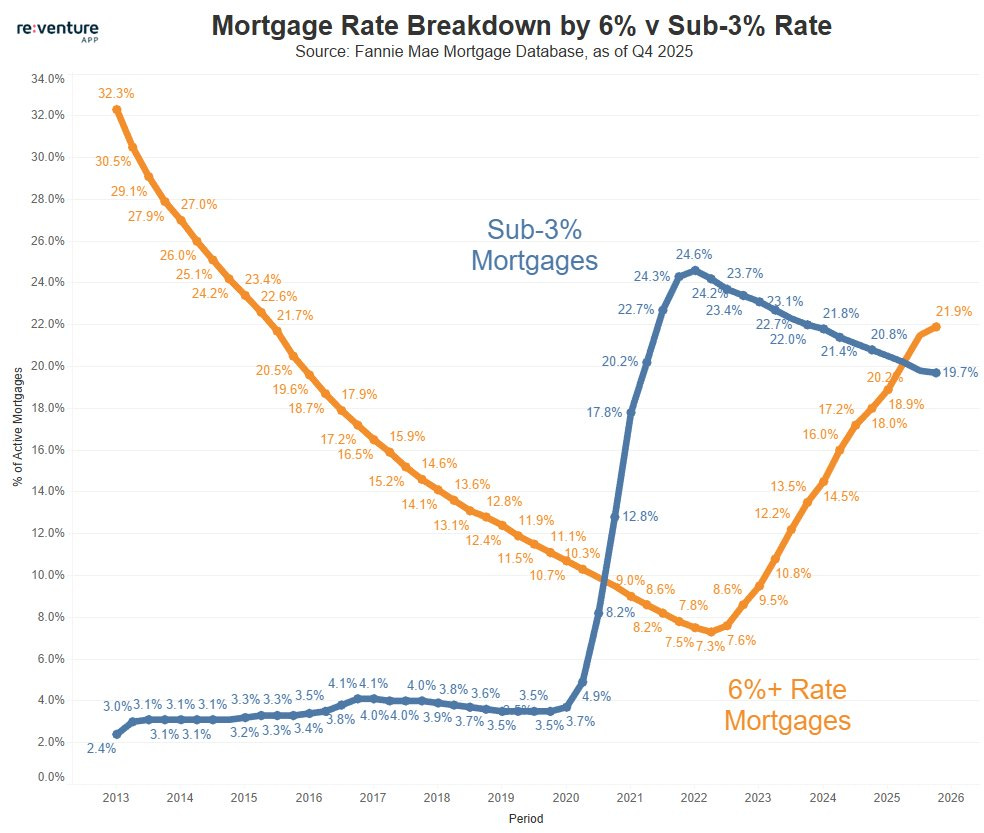

This chart tells the entire story:

Blue line (Sub-3%) → Homeowners who locked in ultra-low rates during 2020–2021

Orange line (6%+) → Buyers dealing with today’s higher rates

Look at the shift:

Sub-3% mortgages surged from ~3% to ~25%

6%+ mortgages dropped sharply… then came roaring back

Today, we have a market split in two.

The “Golden Handcuffs” Effect

If you have a 2.75% mortgage… why would you ever give that up?

Selling your home today likely means:

Taking on a 6–7% mortgage

A much higher monthly payment

Less house for the same budget

So what do people do? They stay.

Why Inventory Is So Low

This is the key dynamic:

Millions of homeowners are locked into ultra-low rates

They have no incentive to sell

New listings stay limited

Even as demand cools… supply stays even tighter.

That’s why prices haven’t dropped the way many expected

Why the Market Feels Frozen

We now have two different realities:

Existing homeowners → sitting on historically cheap debt

New buyers → facing today’s rates

Meanwhile:

Refinancing has dried up

Fewer people are moving

Transactions are down

Higher rates didn’t crash housing. They slowed it down.

What Happens Next?

Even if rates fall:

A homeowner at 3% isn’t rushing into 5–6%

The lock-in effect doesn’t disappear quickly

Supply likely stays constrained

This isn’t temporary. It’s structural.

If You Want to Go Deeper

We’ve been building this theme over time:

The Bottom Line

The housing market isn’t broken.

It’s stuck between two worlds:

Yesterday’s ultra-low rates

Today’s higher-rate reality

And until that gap closes… don’t expect a “normal” housing market anytime soon.