Taxes Don’t Have to Be Complicated

Understanding brackets, deductions, and why planning ahead matters

Most people believe that if they move into a higher tax bracket, all of their income suddenly gets taxed at that higher rate.

That’s NOT how the system works.

That misunderstanding leads to unnecessary fear around raises, bonuses, and saving more.

Let’s walk through taxes the same way we explain them to clients at Sandbox: simple, practical, and without jargon.

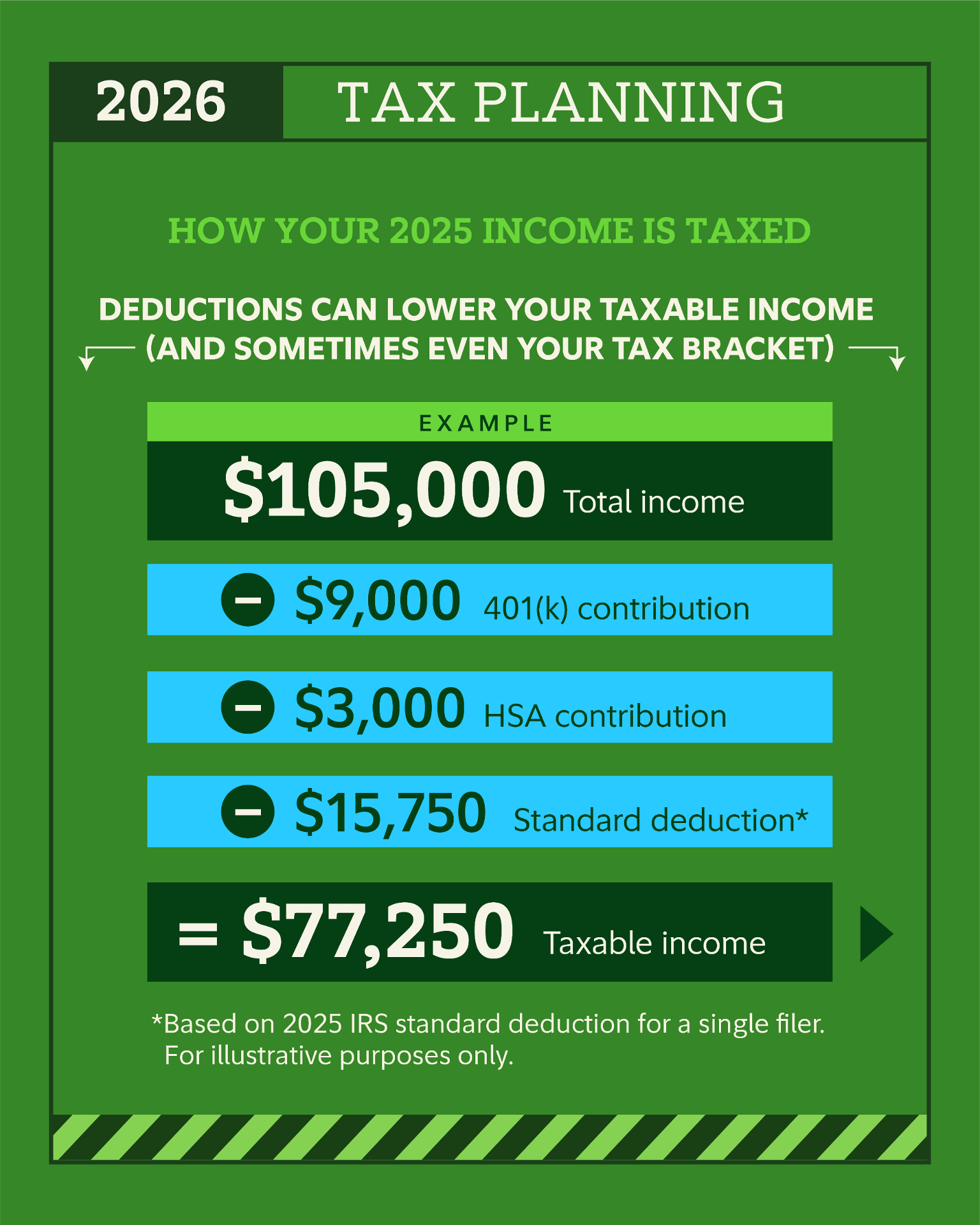

Step 1: Start With Your Total Income

Your total income includes things like:

Salary or wages

Bonuses and commissions

Self-employment income

Interest and dividends

This is your gross income.

But it’s not what the IRS actually taxes.

Step 2: Subtract Deductions

Certain contributions and deductions reduce how much of your income is even subject to tax:

Traditional 401(k) contributions

HSA contributions

Standard deduction (or itemized deductions)

In this example, you earned $105,000 but the IRS only taxes $77,250.

That’s the difference planning.

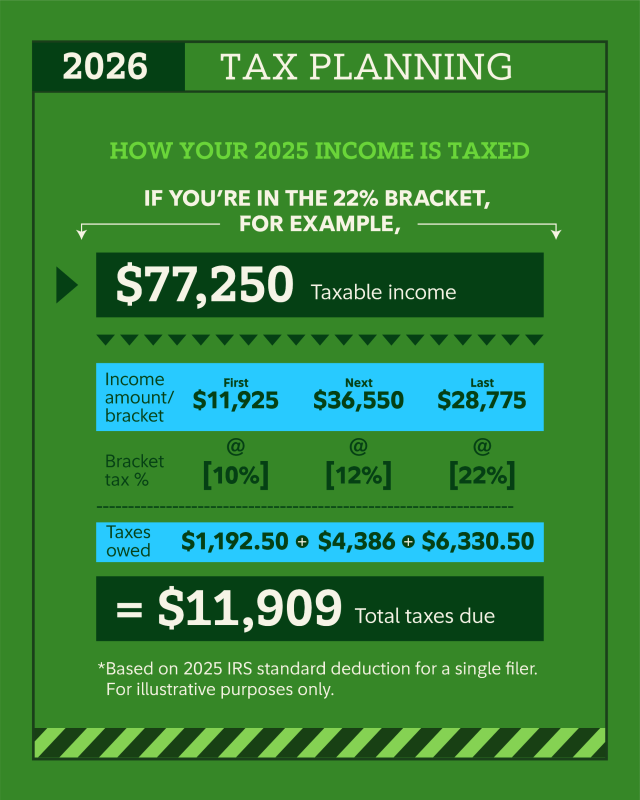

Step 3: How Tax Brackets Actually Work

Tax brackets are layers, not a single flat rate.

Think of them like buckets stacked on top of each other:

The first layer is taxed at 10%

The next layer at 12%

The next layer at 22%

And so on

Only the dollars inside each bucket are taxed at that bucket’s rate.

Not your entire income.

Step 4: A Simple Bracket Example

Using the $77,250 taxable income example:

First $11,925 taxed at 10% → $1,192.50

Next $36,550 taxed at 12% → $4,386

Remaining $28,775 taxed at 22% → $6,330.50

Total federal tax ≈ $11,909

Even though you’re “in the 22% bracket,” most of your money is taxed at lower rates.

2026 Federal Income Tax Brackets

Under current law, several provisions from the 2018 tax cuts are scheduled to expire after 2025.

That means individual income tax brackets are expected to reset to a higher, pre-2018 structure in 2026.

What this means in plain English:

Many households may see portions of their income taxed at higher marginal rates in 2026 and beyond — even if their income doesn’t change.

Not overnight catastrophic. But meaningful over time.

Why This Matters for Planning

When future tax rates may be higher, today’s lower brackets become more valuable.

That creates opportunities to:

Consider Roth conversions

Re-evaluate Roth vs. Traditional contributions

Be intentional about timing income and deductions

Use charitable strategies more efficiently (Donor-Advised Funds, Qualified Charitable Distributions, bunching, etc.)

Plan around employee stock compensation (RSUs, ESPPs, ISO/NSO exercise timing, withholding, and concentration risk)

Build tax diversification across account types

The goal isn’t to predict legislation.

The goal is to avoid being trapped with all of your money in one tax bucket.

A Simple Way to Think About It

You can’t control tax law.

You can’t control markets.

But you can control:

Where you save

How your accounts are structured

Which tax buckets your money lives in

That’s real planning and that’s how you keep more of what you earn.

Illustrations based on 2025 IRS standard deduction for single filers. Projected 2026 brackets assume expiration of current TCJA provisions. Income thresholds shown are estimates and for illustrative purposes only. Individual circumstances vary. Consult your tax professional.

Source: How do tax brackets work? | How do taxes work? | Fidelity