Retirement’s Most Overlooked Expense

What healthcare really costs in retirement

It’s not travel.

It’s not housing.

It’s healthcare.

And for many retirees, it’s the one cost that quietly disrupts an otherwise well-built plan. According to recent research from Fidelity:

A 65-year-old retiring today is expected to spend $172,500 on healthcare in retirement.

That’s not a worst-case scenario.

That’s the average.

Where the Money Actually Goes

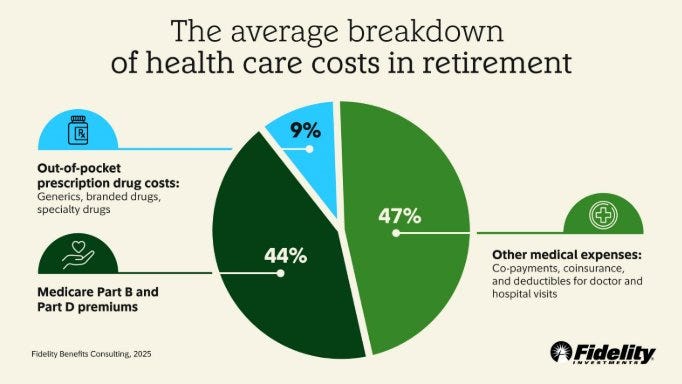

What surprises most people isn’t just the total, it’s the composition.

Nearly half of healthcare costs in retirement come from general medical expenses like co-pays, coinsurance, and deductibles.

Another large portion? Medicare premiums.

And then there are prescription drug costs, which can vary widely depending on health and coverage.

But here’s what that number doesn’t include:

Long-term care

Most dental and vision expenses

Unexpected or catastrophic health events

Which means the real number for many families is… higher.

The Real Risk Isn’t Just the Cost

It’s the timing.

Healthcare costs don’t show up evenly.

They tend to:

Spike later in life

Coincide with reduced flexibility

Hit when portfolios are more vulnerable to withdrawals

This creates a dangerous combination: higher expenses + less time to recover.

Where Most Plans Fall Short

As a financial planner, I see this all the time:

People build thoughtful retirement plans around:

Income

Lifestyle

Travel

Legacy

But healthcare?

It’s often treated as a line item and not a risk.

And that’s where plans begin to crack.

How to Plan for It (The Right Way)

This isn’t about guessing the exact number.

It’s about building a plan that can absorb the uncertainty.

Here’s how we think about it:

1. Stress Test the Plan

Run scenarios that assume:

Higher-than-average healthcare costs

Earlier or more frequent withdrawals

Inflation specifically tied to healthcare (not just CPI)

2. Use the Right Buckets

Not all dollars should be treated the same.

Tax-free accounts (Roth) → ideal for unexpected or large healthcare costs

HSAs (if available) → triple tax advantage, purpose-built for this

Taxable accounts → flexibility for ongoing expenses

3. Plan for Long-Term Care

Long-term care insurance isn’t right for everyone.

But the conversation should start early.

This is something we begin discussing with clients in their 50s, when there are still options, flexibility, and time to plan intentionally.

Because by the time many people start looking into long-term care…

It’s too late

It’s too expensive

Or it’s no longer available

You don’t have to buy a policy. But you do need a plan.

Whether that means:

Self-funding

Hybrid policies

Or earmarking specific assets

The key is making the decision early and on your terms.

Ignoring it is still a decision, just not a good one.

4. Protect the Downside

Healthcare costs become most dangerous during:

Market downturns

Early retirement years (sequence risk)

This is where portfolio structure matters:

Cash buffers

Income layering

Diversification beyond just stocks

5. Revisit the Plan Regularly

Healthcare is not static.

Costs, coverage, and personal health evolve.

Your plan should too.

The Bottom Line

Retirement isn’t just about having enough.

It’s about protecting what you’ve built from the risks that are hardest to predict.

Healthcare is one of them.

And for many families, it’s the difference between:

A plan that works on paper

And a plan that works in real life

If you’re not sure how healthcare fits into your retirement plan, it’s worth a conversation.

Because the goal isn’t just to retire.

It’s to stay retired, comfortably and confidently.

At Sandbox, we help you do exactly that, so you can live more and worry less.