How to Turn RSUs Into Tax-Free Retirement Growth

RSU to a Mega Backdoor Roth

If you receive Restricted Stock Units (RSUs) from your employer, you might be sitting on a powerful but often underutilized opportunity.

Instead of letting those shares sit in a single stock, you can use them to build something far more valuable: tax-free retirement growth.

The Strategy at a Glance

Here’s the game plan:

RSUs vest → you’re taxed on the value

Sell the shares right away → turn concentrated stock into cash

Use the cash to make after-tax contributions to your 401(k) (if your plan allows)

Convert that money into a Roth account

Let it grow tax-free for life

Simple. Smart. Effective.

What Are RSUs?

Restricted Stock Units (RSU) are a form of compensation. When they vest, their value is taxed as ordinary income, whether you sell the shares or not.

After that, they’re just like any other investment.

And for most people, it’s a very concentrated one, tied to the same company that pays their salary.

Why Sell Them?

Holding company stock after it vests can provide upside growth or become a concentrated risky asset.

What if the stock drops 20% next quarter? Or 50%?

Note: We have seen these declines in many technology and software stocks over the past 6 months, with many historic examples of companies that have gone out of business and seen their stocks go to zero.

By selling at the vest date, you:

Lock in the value you’ve earned

Reduce risk from a single stock

Create cash to use more strategically

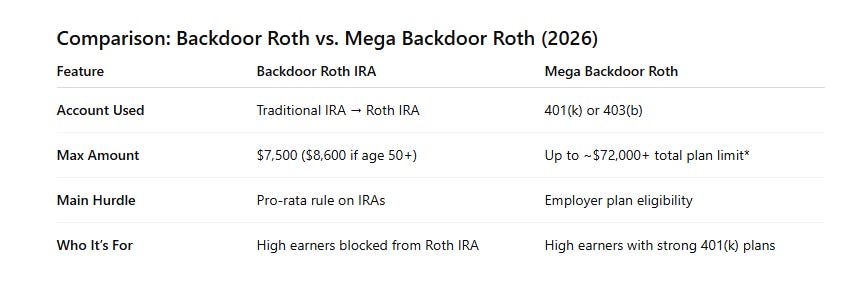

Enter the Mega Backdoor Roth

Most people know about Roth IRAs but income limits prevent high earners from contributing directly. That’s where the Mega Backdoor Roth comes in.

Some 401(k) plans allow you to:

Make after-tax contributions beyond your normal limits

Then convert that money into a Roth account

This allows you to move significantly more money into a Roth than traditional limits allow. But not all 401(k) plans offer this.

Step-by-Step Flow

RSUs Vest

Sell Immediately → Cash in Hand

Contribute After-Tax to 401(k)

Convert to Roth account

Growth becomes Tax-Free

A Few Important Notes

Not all 401(k) plans allow this strategy. Check with your plan administrator.

RSU sales may trigger capital gains if you wait too long after vesting.

Final Thought

You worked hard for those RSUs.

Don’t let them sit in one stock or get lost in a tax-heavy strategy unless that’s part of your financial plan.

With the right approach, you can turn that compensation into a long-term, tax-free asset.

That’s the difference between just getting paid… and making your money work smarter.

The Mega Backdoor Roth is one of the most powerful strategies available to high earners and using your RSUs to fuel it is a smart financial planning strategy.

Sandbox is available to review this strategy and how it fits into your financial plan—we’re here to help you move forward with clarity and confidence. Contact us to start the conversation.