How Taxes Actually Work (Most People Get This Wrong)

The basics that quietly impact your wealth every year

Taxes aren’t just something you deal with once a year.

They influence:

How you invest

When you sell

How you structure income

And ultimately… how much wealth you keep

Yet most people are making decisions based on a few half-truths.

Let’s clear up the ones I see most often.

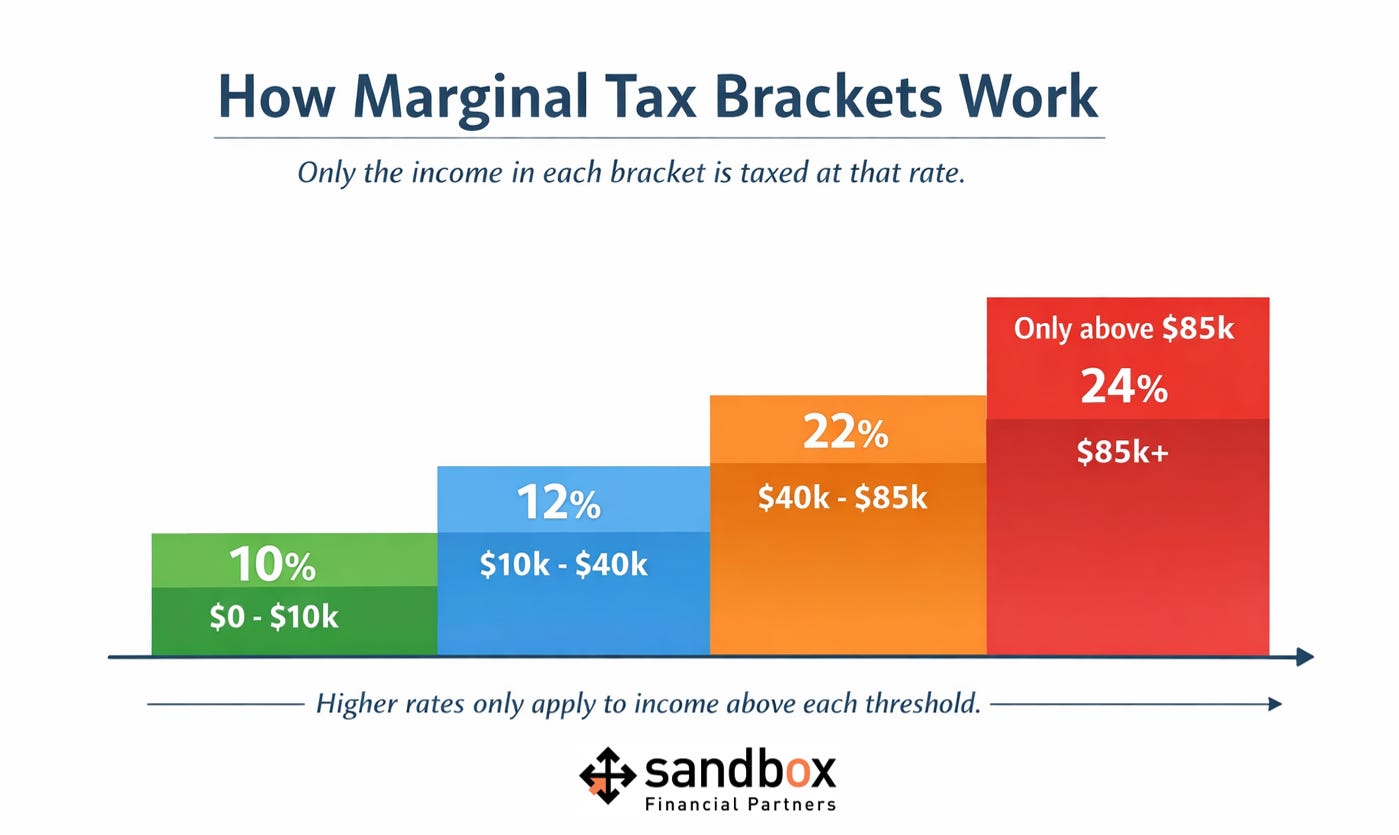

1. Not All Your Income Is Taxed the Same

One of the biggest misconceptions:

“I don’t want to earn more because I’ll move into a higher tax bracket.”

That’s NOT how it works.

The U.S. tax system is marginal, meaning:

Your first dollars are taxed at lower rates

Only the income above certain thresholds gets taxed at higher rates

So earning more money doesn’t “push all your income” into a higher rate.

It just means the next dollar is taxed differently.

👉 Example:

If you move into a 24% bracket, only the income above that threshold is taxed at 24% — not everything you earn.

More income means more take-home.

2. The System Is Designed to Be Progressive

As income increases, taxes increase gradually, not all at once.

You don’t fall off a cliff into a worse outcome.

You climb a staircase.

👉 Example:

If you earn $100,000, your income is taxed in layers:

First portion at 10%

Next at 12%

Next at 22%

Next at 24% and so on

Only the income within each layer gets taxed at that rate.

Think of it like stacking blocks—not flipping a switch.

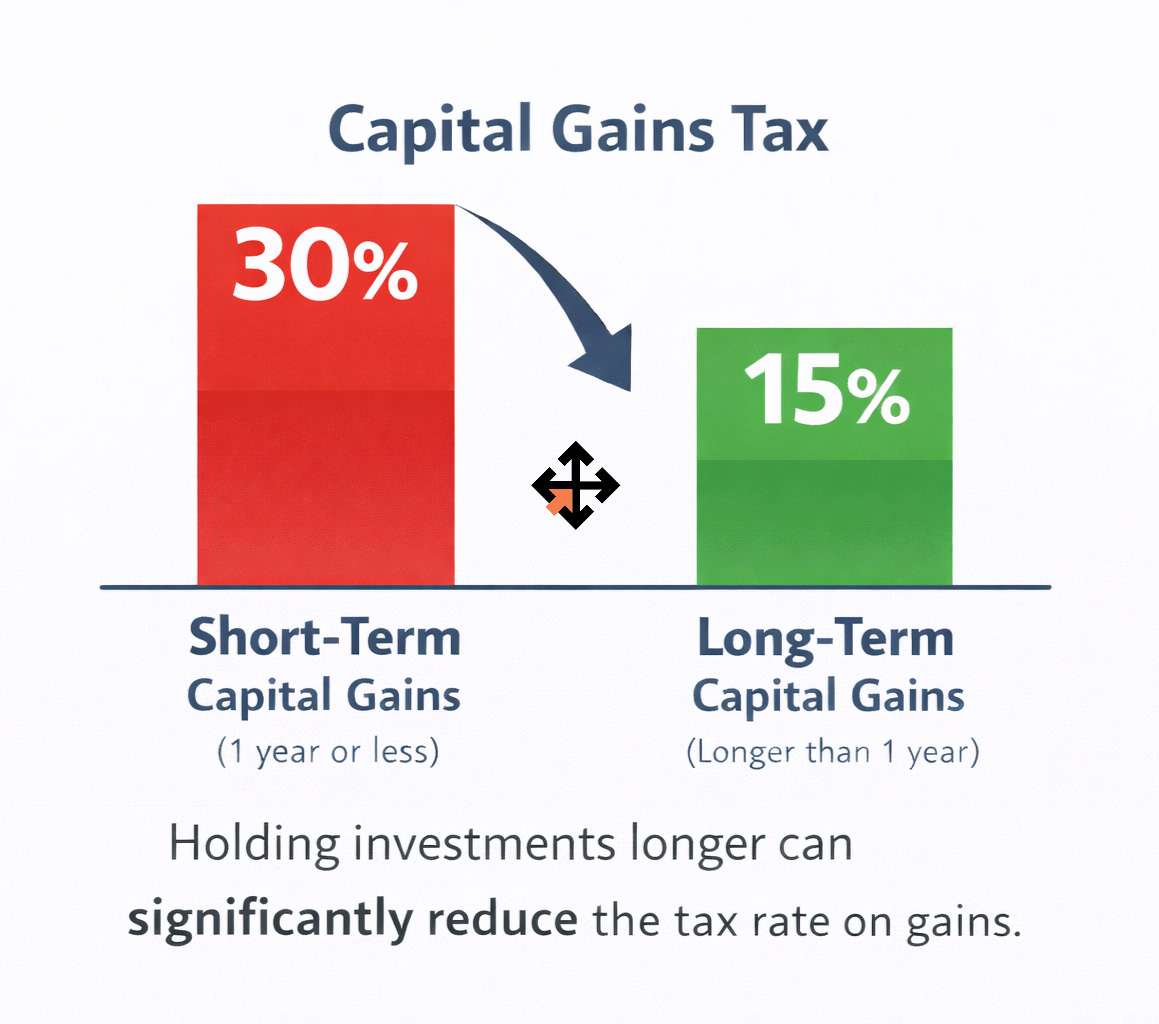

3. Time Changes How Investments Are Taxed

Not all investment gains are treated equally.

Short-term gains (≤ 1 year) → taxed like ordinary income

Long-term gains (> 1 year) → taxed at lower, preferential rates

And for higher earners, there’s also the 3.8% Net Investment Income Tax (NIIT) layered on top.

👉 Example:

Sell a stock after 11 months → taxed at your income rate (could be 30%+).

Sell that same stock after 13 months → potentially taxed closer to 15–20%.

Same investment. Different outcome.

Patience isn’t just a virtue—it’s a tax strategy.

4. Deductions and Credits Are Not the Same

This one trips people up all the time.

A deduction reduces your taxable income

A credit reduces your tax bill directly

👉 Example:

A $10,000 deduction might save you ~$2,400 if you’re in a 24% bracket.

A $10,000 credit saves you the full $10,000.

Big difference.

5. The Best Tax Move Isn’t Always the Lowest Tax Today

This is where real planning happens.

Many strategies that reduce taxes today can increase total taxes over your lifetime.

👉 Example:

Two people earn $150,000:

One uses pre-tax accounts to save on taxes today

The other uses Roth accounts and pays taxes now

Years later, if tax rates are higher or their income increases, the Roth investor may come out ahead long-term.

Good planning doesn’t ask: “What saves me the most this year?”

It asks: “What minimizes taxes over the next 10, 20, 30 years?”

6. Tax Savings Shouldn’t Drive Every Decision

I see this constantly—especially with business owners.

A decision gets justified with:

“But it’s a write-off.”

👉 Example:

Buy an $80,000 vehicle.

Save ~$25,000 in taxes.

You’re still down $55,000.

The tax benefit helped—but it didn’t make it a good decision.

7. Most People Don’t Actually Benefit From Itemizing

Because of today’s standard deduction, many people don’t receive additional tax benefits from:

Mortgage interest

Charitable giving

State and local taxes

👉 Example:

If your deductions total $27,000 but the standard deduction is ~$29,000…

You take the standard deduction and those expenses did NOT reduce your taxes further.

The Bottom Line

Taxes matter. A lot.

For high earners and high net worth families, they’re one of the most controllable levers in a financial plan.

But here’s the key: Tax strategy should support your life, not dictate it.

The best plans don’t just minimize taxes this year.

They create clarity, flexibility, and confidence over decades.

If you’re making big decisions around income, investments, or business structure, it’s worth stepping back and looking at the full picture.

Because when it comes to taxes:

Short-term thinking is expensive.

Long-term planning is where the real value lives.