529 Plans Aren't Just for College Anymore

New rules have expanded what these accounts can pay for.

Ask most people what a 529 plan is, and they’ll tell you it’s a college savings account.

That’s true—but it’s no longer the whole story.

Over the past several years, lawmakers have expanded what 529 plans can be used for. What was once primarily a tool for college tuition has evolved into a much more flexible education and career planning account.

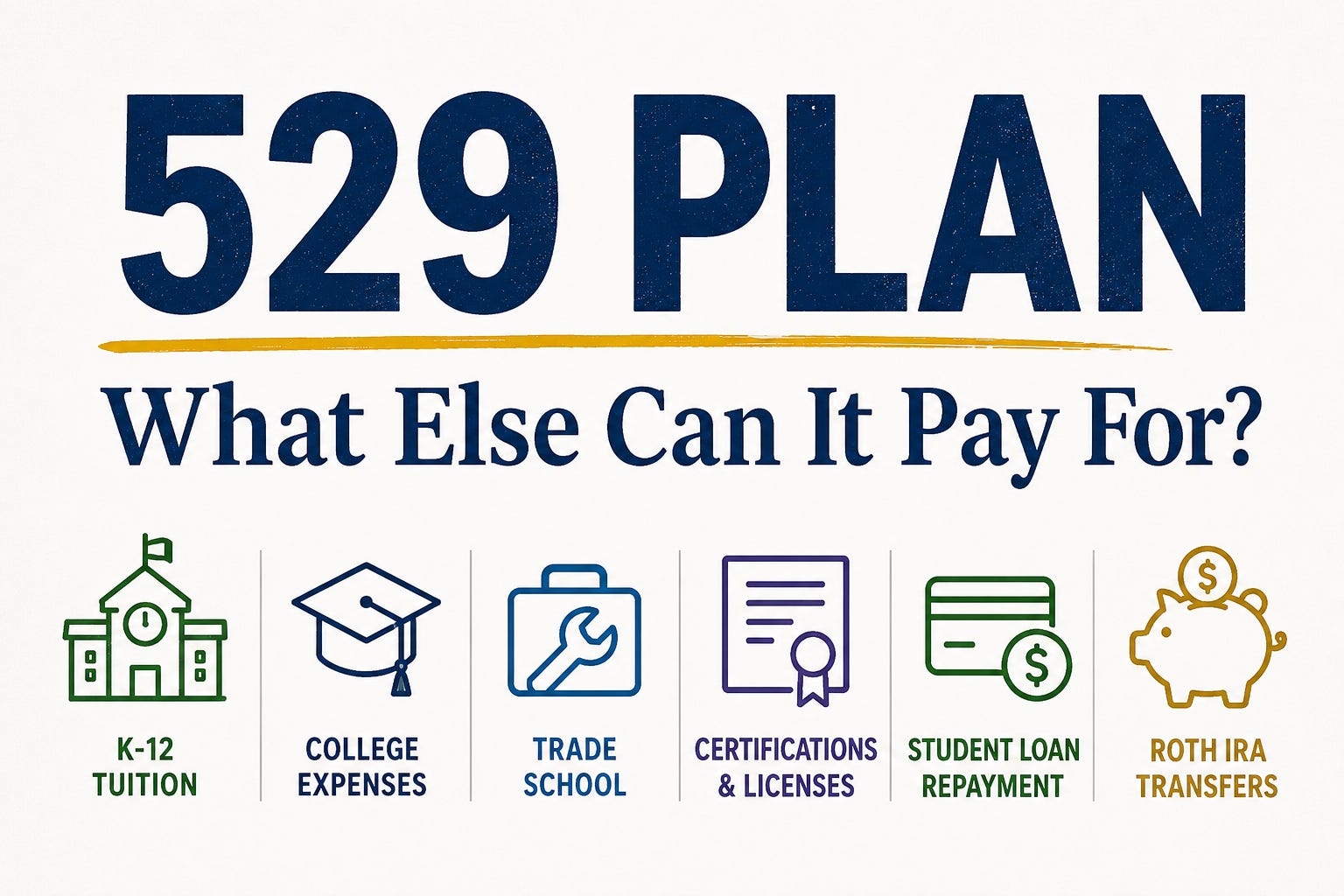

Today, a 529 plan may help fund everything from private school tuition and trade schools to professional certifications, student loan repayment, and even a Roth IRA.

That’s a much bigger toolbox than most families realize.

That’s also why the fear of “overfunding” a 529 plan isn’t as significant as it once was.

Before College

Many parents are familiar with the ability to use a 529 plan for private school tuition, but recent changes have expanded the opportunities even further.

Depending on your situation, a 529 plan may help cover:

K-12 private school tuition (up to $20,000 per year)

Homeschool curriculum and instructional materials

Educational software and online learning programs

Certain tutoring and testing expenses

For families considering private school or homeschooling, these provisions can make a meaningful difference.

During College

This is the traditional use of a 529 plan, but many families still overlook some of the expenses that may qualify.

In addition to tuition, 529 assets can often be used for:

Room and board

Meal plans

Computers and laptops

Internet access

Required software

Books and supplies

For many students, housing and living expenses can rival the cost of tuition itself.

After College

This is where things get especially interesting.

Recent rule changes have expanded the use of 529 plans for certain workforce training and credentialing programs.

Depending on the program, 529 funds may now be used for:

Professional certifications

Licensing programs

Trade school credentials

Apprenticeship programs

Industry-recognized certifications

Certain continuing education requirements

Think beyond the traditional four-year degree.

Future CFP® professionals, CPAs, lawyers, nurses, electricians, cybersecurity specialists, project managers, and countless other professionals may benefit from these expanded rules.

Student Loans

Families with unused 529 balances have another option.

Up to $10,000 can be used toward qualified student loan repayment, helping graduates reduce debt and improve financial flexibility.

A Roth IRA Backup Plan

One of the most significant recent changes addresses a concern many parents have had for years:

“What if we save too much?”

Under current rules, certain unused 529 assets may be transferred to a Roth IRA for the beneficiary, subject to account age requirements, annual contribution limits, earned income requirements, and other rules.

While not unlimited, it provides families with an important backup plan that didn’t exist a decade ago.

The Bottom Line

One of the biggest mistakes I see is families avoiding a 529 plan because they’re worried their child may not attend college or won’t use all of the money.

That’s an understandable concern.

But today’s 529 plans are far more flexible than they once were.

Whether a child chooses private school, a four-year university, a trade program, law school, a professional certification, or a completely different path, today’s 529 plan offers more flexibility than ever before.

The modern 529 plan isn’t just designed to help someone get into a career. It can help them build one.

This article is for educational purposes only and should not be considered tax, legal, or investment advice. Rules vary by state and individual circumstances. Consult your tax advisor before making decisions regarding 529 plan distributions.